When you purchase your first home, you will be inundated with terms you may find difficult to understand. This is not your fault. The American educational system—even at the collegiate level—is woefully deficient when it comes to preparing us for real-world financial situations. Fortunately, the internet allows us to educate ourselves using independent sources that feel no need to mislead us. This is an invaluable resource.

One area that both first time and repeat home-buyers or refinance borrowers have difficulty understanding is the concept of mortgage points. One point is exactly 1-percent of the total loan amount. That does not mean it is 1-percent of the total cost of the house, just that of the actual loan you’ve taken.

In this post, we will discuss the 2 types of mortgage points…

- Discount points

- Origination points

…and also whether purchasing points is the right choice for you.

What Are Discount Mortgage Points?

The most commonly used mortgage points are known as discount points. These points are bought at closing for 1-percent of the total loan amount. If you take out a $300,000 loan, you will pay $3,000 per discount point. Each discount point normally equates to roughly a reduction of 0.25-percent on your interest rate. This is general rule and can vary from lender to lender. If you choose to buy 4 points at $12,000, your interest rate over the life of your loan can be reduced by as much as 1-percent, and that can save you a significant amount of money for a relatively modest initial investment.

Because they’re a form of prepaid interest, discount mortgage points also have the benefit of being an itemized deduction on your tax return.

What Are Origination Mortgage Points?

Origination points are non-tax-deductible points that are purchased. Essentially, they cover the cost of processing your loan—evaluating your credit worthiness, appraisal, approval process, etc. They are still 1-percent of your mortgage total, though many lenders are willing to negotiate this fee. They have no real effect on the total amount you will pay on your mortgage. These points are simply fees which go to the lender or broker.

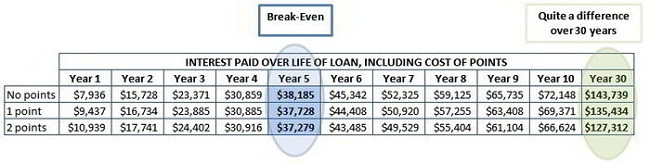

Origination points have very little to do with the long term cost of your mortgage, so we will focus the remainder of this post on discount mortgage points and at what point it is wise to make an investment at purchase points on your home mortgage. In the chart found below, we are going to stick with the initial loan value of $200,000 and an interest rate of 4.0-percent over 30 years. These are only illustrative rates, your actual rate & fees could very well be different.

As you can easily see, year 5 is when you break even and any amount of discount mortgage points begin to pay

dividends; so if you choose to purchase discount points when you apply for a mortgage, you should intend to stay in your home for at least 6 years. Make sure you are moving into a home large enough for your growing family, in a wonderful neighborhood, in a city you absolutely love before investing in mortgage discount points.

A final note – the scenario changes depending on your credit profile and percentage of equity in your house – points can be cheaper or more expensive depending on these and other factors. Therefore, always get an expert opinion before deciding whether points make sense or not.